AUGUSTA, Ga. — The Masters green coat that came into vogue in the late 1930s has become what amounts to the world’s most recognizable reversible jacket. Augusta National Golf Club members wear theirs on the grounds to make themselves visible to tournament patrons seeking guidance on the course. And the reigning Masters champion wears it to make himself visible outside the club’s gates to anyone in search of a connection.

The winner is allowed to remove the jacket, one of the most classic prizes in sports, from the Augusta National grounds only during the year of his reign. Gary Player said that after he won the 1961 Masters, he took the jacket home to South Africa, “hung it up with my honors blazer from other sports at school in a plastic bag,” and forgot about it.

The next year, Player lost to Arnold Palmer in a three-way playoff and returned home. Shortly thereafter, he received a call from Clifford Roberts, one of Augusta National’s founders, reminding him that he needed to return his jacket to the club.

Only one jacket is allowed to circulate in public in any given year, heightening its mystique.

“It’s very rare that it makes appearances anywhere,” said the 2013 champion Adam Scott, who treated his green jacket as his plus-one.

It was on his arm in his native Australia, in his homes in Switzerland and the Bahamas, and at every organized dinner or informal party to celebrate his becoming the first golfer from his country to enjoy the pleasure of the jacket’s company.

To the club members, the bright green garment, made of tropical-weight wool and polyester, with a rayon lining, an Augusta National logo patch on the left breast pocket and brass buttons, is a status symbol.

On Scott and the other players who have worn it over the decades, the jacket represents something more powerful. It is a conversation piece, a cover-up that causes people to display their joy and awe.

“It’s been mostly what anyone talks to me about in the last 12 months since the Masters,” Scott said, adding: “It always gets an incredible reaction if there are golfers in the room. If they are not golfers, they wonder why I’m wearing a very bright green jacket, I think.”

In airports, at cocktail parties and waist-deep in the Pacific surf, strangers have shared with Scott where they were last April when he defeated the Argentine Ángel Cabrera on the second playoff hole.

“People were just as excited to tell me where they were when I won and their story as I was talking about the Masters,” Scott said. He laughed. “So I got cut off a lot of times.”

Nick Faldo heard a story when he wore his green jacket on a talk show in Britain in 1989, after winning the first of his back-to-back titles. The other guest was the actor Sean Connery.

Faldo said: “The most amazing thing about Sean Connery, if I can tell the story he told me then, is when he was James Bond back in the early ’60s and everyone was inviting him to everything, to be a member of every club in the world, he got his invitation to be a member of Augusta National and threw it in the bin. He didn’t know what it was.

The jacket’s hue, called Masters green, proved ideal for color television, which captured it, and the tournament, in all its radiance. If the jackets could talk, oh, the tales they could tell. The 2011 champion Charl Schwartzel left his in the back seat of a car driven by a tournament volunteer.

“The car drove off, but the guy was honest enough to bring it back,” Schwartzel said, adding: “It could have been worse. If you left it in a taxi, then they would have gone with the jacket.”

Phil Mickelson, the winner of three Masters jackets, has worn one on the floor of the New York Stock Exchange and in the drive-through of a Krispy Kreme doughnut shop, where he was photographed by the store manager.

“I think it’s such a cool thing to be able to travel around with it,” Mickelson said, adding, “That’s a really special thing that the club allows the champion to do.”

Mike Weir, who in 2003 became the first Masters winner from Canada, wore his jacket to drop the puck at a Toronto Maple Leafs playoff game against Philadelphia and got chills when the players responded by tapping their sticks on the ice.

Like Cinderella’s glass slipper, the green jacket has a transformative effect on those able to slip into one. The former N.F.L. receiver Andre Reed and the retired baseball slugger Ken Griffey Jr., who never won their professional sports’ ultimate prizes, took turns trying on Mark O’Meara’s green jacket at a party in his honor after his 1998 victory.

“Their eyes lit up,” O’Meara said.

Trevor Immelman, who won 10 years after O’Meara, was in an airport in Japan when a group of businessmen saw the green jacket draped over his arm and started crying.

“I think the awe is the same as when I’ve touched an Olympic gold medal or Stanley Cup,” Immelman said. “It’s the pinnacle of sport, really.”

Immelman’s countryman, Player, who won three Masters titles from 1961 to 1978, said he had never worn his jacket in public. “Not even at my dinner table with my 13 grandchildren,” he said.

Jack Nicklaus, a six-time winner, said, “I’ve never taken it off the club grounds.”

Fuzzy Zoeller, who won in 1979, said he had worn his jacket during a parade in his honor in his hometown, New Albany, Ind. “And that was about it,” he said.

Zoeller is reunited with his jacket every year when he returns to Augusta National for the Champions Dinner and the par-3 contest. “There is something magical,” he said, about wearing it on the grounds during the tournament. “People want to walk up and feel it, touch it.”

During his yearlong reign, Schwartzel, like Scott, squired his green jacket all over the world.

“Any opportunity I had to wear it, I would wear it,” he said. “Any functions, I would rather wear the green jacket than a suit. It went down a lot better.”

Immelman said, “I think the last few years, the champions have done a great job of showing it off a little more.”

He added, “If I had the chance to wear it again, I’d do more with it.”

Scott never took the jacket to some spots he treasures in Australia, one reason he is eager to keep it another year.

“There were a lot more places to wear it than I had nights up my sleeve,” said Scott, who is six shots off the pace after 54 holes. “The only way to deal with that is winning again.”

Even if your overall cash-flow situation is good, but you still need to cover a short-term deficit, today’s still-strict credit environment often won’t allow you to take out a loan. More than likely, your only option would be an untapped home equity line of credit or a generous relative. If that’s the case, great. If not, you may be able to turn to a surprising source for some help: the taxman.

What you do is simply postpone some federal income tax payments that you would otherwise make to the IRS via estimated tax installments. You don’t need the government’s permission. You just do it and then make up the difference later. Of course, the IRS will charge interest on the difference between what you should have paid in for each installment and what you actually paid. However, the current interest rate on estimated tax underpayments is only 3%. While the rate can potentially change each quarter, it will probably remain at a reasonable level for a while.

The IRS calls the interest on estimated tax underpayments a “penalty.” But since the current interest rate is only 3%, it’s not really a penalty. In fact it’s actually a pretty good deal for someone with a short-term cash crisis.

Note: If you are a salaried employee, you must pay in federal income taxes via payroll withholding. You may be able to adjust the withholding downward a bit for the rest of this year by turning in a revised Form W-4 to your employer. However, the strategy of borrowing from the IRS is basically unavailable to you. Sorry.

Estimated Taxes:

There is no federal income tax withholding on income from self-employment activities conducted via sole proprietorships, partnerships, or LLCs. Nor is there generally any required federal income tax withholding on interest income, dividends, capital gains, Social Security benefits, pension payments, or taxable retirement account withdrawals. Instead those with income from these sources are expected to make four installment payments of estimated taxes for each year. The installments for the 2012 tax year are due on Apr. 17, June 15 and Sept. 17 of this year, and Jan. 15 of 2013. Obviously the first date has since passed, but the next three are still in the future. So you can work with the installments due on those dates by paying in less than you owe or even nothing at all.

Borrowing from the IRS in this fashion is only a short-term fix. By no later than April 15th of next year, you must catch up for any estimated tax payment shortfalls for the 2012 tax year. If you don’t, the IRS will start charging additional interest of half a percent per month on the shortfall, which equates to a 6% annual rate. That 6% is on top of the “regular” interest charge, which is currently only 3%. So you could be looking at a rate of 9% or maybe more. In any case, owing the IRS for 2012 taxes after April 15th of next year is just not a good position to be in. So, if you are not ready, willing, and able to pay up by that date, this is not a good option for you. You do not, however have to wait until April 15th to catch up. You can do so as soon as you are able and that is the recommendation.

Are you LinkedIn? If not, try expanding your horizons outside that of Facebook. Indeed, LinkedIn has more than 100 million members, including executives from every Fortune 500 company. LinkedIn’s research team recently mined that information to determine the most common names for CEOs. Verdict? Peter, for a man, and Deborah, for a women. But no matter what your name, LinkedIn can take your networking to the next level with just a little effort. Here are the most common ways people aren’t making the most of their presence on the site (and how experts say you can fix that):

Having A Vague Headline

Say your current title is marketing manager. Many people naturally leave that as their headline, which is a huge error because it says nothing about what you actually do, says career coach Kimberly Schneiderman. Instead: “Use a headline statement that really describes your expertise and talent, like ‘Executive-level Product Strategist’ or ‘Hospitality Executive — Expertise in Franchise, Operations, & Change Management,'” suggests Schneiderman. Then further develop it: “Create a summary about your career that fully describes your passion for your work, your impact in your company or companies, and your professional focus. People in an open job search can map out the kinds of opportunities they are pursuing next. Make it about 3 paragraphs and write in 1st-person using ‘I’ statements,” says Schneiderman.

Maintaining A Passive Profile

Filling out an attractive profile is just the beginning. “Most people create a LinkedIn profile, but then don’t take advantage of potential connections that might be available through their existing network,” says career consultant Shawn Graham, author of Courting Your Career. His suggestions: regularly identify and reach out to potential contacts, use status updates to congratulate those contacts on their successes, and consistently review the “People You May Know” section to identify additional connections.

Not Trying New Tools Branding expert Dan Schawbel says that a major mistake is not taking advantage of the many tools Linkedin has to offer. His tips include connecting with someone you have no connection with by joining a LinkedIn Group they’re active in, using a 1st degree contact to gain access to 2nd and 3rd degree ones, and using apps like SlideShare to connect with even more people. And don’t forget to take your toolbox on the go: “The LinkedIn mobile application allows you to transfer contact details electronically,” says Schawbel. A new one has just been released for the Droid.

Networking Only When You Need Something

Schawbel also reminds people that networking on LinkedIn is no different than networking in real life. You still want to give more than you receive, particularly when asking for a recommendation: “The best way to get recommendations on LinkedIn is to give one first,” says Schawbel.

When it comes to retirement, there are many things to consider: taxes rates, vacations, and maybe where you plan on living. But experts are saying that there are 2 major obstacles that must be factored into your plans: the old notion that, “hey, I can work later in life” and make up for my savings then, and the diagnosis, either by you or a loved one, with Alzheimer’s disease. Research has indicated that many Americans plan to keep working as a way to make up for not having saved enough or invested wisely enough for retirement, or as a way to keep health insurance. These are both good reasons to continue working, however, many companies, according to the unemployment reports, are still laying off, specifically, 55 years and older employees. No assumptions can be made that a job will be there for you when you reach that age or are coming up to that age, so you should look at other options now. You should speak with a financial adviser, as it is never too late to plan for your retirement, but not doing it at all can prove problematic to your future well-being.

The second possible obstacle is Alzheimer’s disease, either suffered by you or a loved one. It is estimated that around 5.3 million people now suffer from this disease. And the prevalence of Alzheimer’s is supposed to grow by at least 80% by 2025. You don’t have to go on facebook to realize that there is only one degree of separation between you and someone with Alzheimer’s or dementia; and you may also realize that those most affected by this terrible disease are women. When families are faced with this diagnosis, they are often left scrambling and are subject to fall victim to any one or all of these fraudulent practices: medical, financial, and legal. Because of this, understanding that there is a 3-20 yr. lifespan for this disease, and speaking with an estate planner or financial adviser about how to plan for 20 years of dependent care (just in case) is the most responsible financial move you can make. The second most important decision you must make is choosing your beneficiaries and power of attorney(s). The more decisions you take control of now, the less worrying you will have later.

Other than claiming your child as a dependent on your taxes, the two biggest tax breaks that children can provide are the dependent-care credit and the child tax credit. If you pay for babysitting or daycare for a child under 13, you can claim a tax credit if you and your spouse both work or if one parent is a full-time student or disabled. A single parent with earned income is also eligible.

A few other things to make sure you document before you turn your taxes over to your accountant, are that nursery school and kindergarten costs are usually eligible, but private school expenses in first grade or higher are not; overnight camp expenses are not eligible, but day camp expenses are (with some cost restrictions, see your CPA).

Then there is the kiddie tax: Your children are inevitably going to fall into a lower tax bracket, so they will pay less on investments. The kiddie tax enables the first $700 of unearned income for children under 14 years to be considered tax free; the next $700 will only be taxed at his/her rate. All additional income above that will be taxed at the parents’ rate. After age 14, the kiddie tax disappears and all investment income is taxed at the child’s rate. Just remember, when applying for financial aid for college rolls around, investments in your child’s name may make him or her ineligible. Deciding the best ways to invest to provide maximum return and tax breaks can be discussed with your financial adviser.

Section 529 of the tax code established 2 types of higher education investment plans that will also provide you with preferential tax treatment. The 529 college savings plan allows assets in the account to grow and your withdrawals for college expenses to be made tax free. The second type, a 529 prepaid tuition plan, also known as prepaid educational arrangements (PEAs), provides tax-deferred growth on savings for tuition, based on the current cost of that tuition.

Prepaid Educational Arrangements can be purchased in units, usually credit hours or a percentage of the annual tuition fee, or in contracts for 1 to 5 years of tuition. Payments can be made in a lump sum or in installments. The states that administer PEAs guarantee that your investment will, at the very lease, match college tuition increases. For that reason, these plans are typically much more conservative than other types of college savings, so they may not be appropriate for late-stage college saving.

Because PEAs can be purchased for the student by anyone, they allow aunts, uncles, grandparents, and even unrelated benefactors to help with educational costs and, depending on the state, receive a break on their taxes. Most PEAs are transferable to other members of your family, including parents, brothers, sisters, and children if the original beneficiary decides not to attend college. The distributions from the PEAs are not taxed by the Federal government as long as they’re used for tuition and fees. The primary drawback, however, is that states administering these plans usually require that the funds be used for a school in that state. That may be a difficult commitment to make if your child is young and his/her “future” career is pretty much up in the air, although the ability to transfer to another family member gives you one option if plans change.

PEAs are just one of the extensive opportunities for securing your child’s future and typically contain less risk. By meeting with a trusted financial professional and finding out your options, you will move yourself one step closer to helping your child take part in the most important investment of their lives: their education.

The promise to settle all your debts pennies on the dollar sounds like a dream come true for countless consumer and the promise of hundreds of advertisers. Beware. There can be major tax consequences to having your debts forgiven. Once you have your debts canceled, the forgiven balance is considered taxable income on your annual returns. The IRS, unfairly in my opinion, views the forgiven amount as going from a loan you had to repay to income the moment you didn’t have to pay it back. There are certain circumstances in which forgiven debt is not considered income and you should speak to a qualified tax professional to see if you qualify or can qualify for one of these special circumstances. When considering debt forgiveness make sure to consider the effect on your credit score and if it would be the best financial move for you in the long run as well.

Owning a home can pay off at tax time. Take advantage of these home-ownership-related tax deductions and strategies to help lower your tax bill:

Mortgage Interest Deduction

One of the best deductions itemizing homeowners can take advantage of is the mortgage interest deduction, which you claim on Schedule A. To get the mortgage interest deduction, your mortgage must be secured by your home — and your home can be a house, trailer, or boat, as long as you can sleep in it, cook in it, and it has a toilet. Interest you pay on a mortgage of up to $1 million — or $500,000 if you’re married filing separately — is deductible when you use the loan to buy, build, or improve your home.

If you take on another mortgage (including a second mortgage, home equity loan, or home equity line of credit) to improve your home or to buy or build a second home, that counts towards the $1 million limit.

If you use loans secured by your home for other things, like sending your kid(s) to college, you can still deduct the interest on loans up $100,000 ($50,000 for married filing separately) because your home secures the loan.

PMI and FHA Mortgage Insurance Premiums

You can deduct the cost of private mortgage insurance (PMI) as mortgage interest on Schedule A if you itemize your return. The change only applies to loans taken out in 2007 or later. By the way, the 2014 tax season is the last for which you can claim this deduction unless Congress renews it for 2015, which may happen, but is uncertain.

What’s PMI? If you have a mortgage but didn’t put down a fairly good-sized downpayment (usually 20%), the lender requires the mortgage be insured. The premium on that insurance can be deducted, so long as your income is less than $100,000 (or $50,000 for married filing separately). If your adjusted gross income is more than $100,000, your deduction is reduced by 10% for each $1,000 ($500 in the case of a married individual filing a separate return) that your adjusted gross income exceeds $100,000 ($50,000 in the case of a married individual filing a separate return). So, if you make $110,000 or more, you can’t claim the deduction (10% x 10 = 100%).

Besides private mortgage insurance, there’s government insurance from FHA, VA, and the Rural Housing Service. Some of those premiums are paid at closing, and deducting them is complicated. A tax adviser or tax software program can help you calculate this deduction. Also, the rules vary between the agencies.

Prepaid Interest Deduction

Prepaid interest (or points) you paid when you took out your mortgage is generally 100% deductible in the year you paid it along with other mortgage interest. If you refinance your mortgage and use that money for home improvements, any points you pay are also deductible in the same year. But if you refinance to get a better rate or shorten the length of your mortgage, or to use the money for something other than home improvements, such as college tuition, you’ll need to deduct the points over the life of your mortgage. Say you refi into a 10-year mortgage and pay $3,000 in points. You can deduct $300 per year for 10 years.

Property Tax Deduction

You can deduct on Schedule A the real estate property taxes you pay. If you have a mortgage with an escrow account, the amount of real estate property taxes you paid shows up on your annual escrow statement. If you bought a house this year, check your HUD-1 settlement statement to see if you paid any property taxes when you closed the purchase of your house. Those taxes are deductible on Schedule A, too.

Energy-Efficiency Upgrades

If you made your home more energy efficient in 2014, you might qualify for the residential energy tax credit. Tax credits are especially valuable because they let you offset what you owe the IRS dollar for dollar for up to 10% of the amount you spent on certain home energy-efficiency upgrades. The credit carries a lifetime cap of $500 (less for some products), so if you’ve used it in years past, you’ll have to subtract prior tax credits from that $500 limit. Lucky for you, there’s no cap on how much you’ll save on utility bills thanks to your energy-efficiency upgrades.

Among the upgrades that might qualify for the credit: Biomass Stove; Heating ventilation, and air conditioning; Insulation; Roofs (metal and asphalt); Water heaters; Windows, doors, and skylights.

To claim the credit, file IRS Form 5695 with your return.

Vacation Home Tax Deductions

The rules on tax deductions for vacation homes are complicated. Do yourself a favor and keep good records about how and when you use your vacation home.

If you’re the only one using your vacation home (you don’t rent it out for more than 14 days a year), you deduct mortgage interest and real estate taxes on Schedule A.

Rent your vacation home out for more than 14 days and use it yourself fewer than 15 days (or 10% of total rental days, whichever is greater), and it’s treated like a rental property. Your expenses are deducted on Schedule E.

Rent your home for part of the year and use it yourself for more than the greater of 14 days or 10% of the days you rent it and you have to keep track of income, expenses, and allocate them based on how often you used and how often you rented the house.

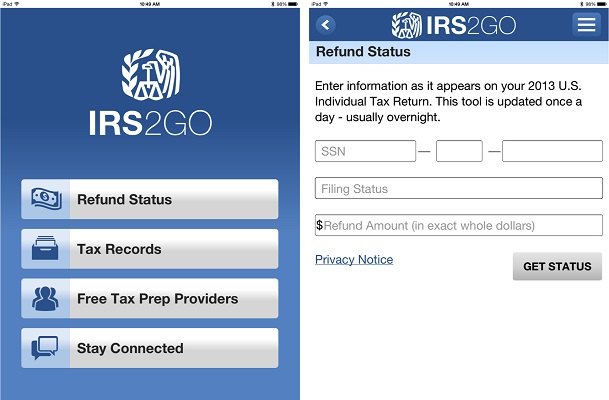

Check Refund Status You can check the status of your federal income tax refund using IRS2Go. Simply enter your Social Security number, which will be masked and encrypted for security purposes, then select your filing status and enter the amount of your anticipated refund from your 2013 tax return. A status tracker has been added so you can see where your tax return is in the process. If you filed your return electronically, you can check your refund status within a 24 hours after we receive your return. If you file a paper tax return, you will need to wait about four weeks to check your refund status because it takes longer to process a paper return.

Tax Records

You can request your tax return or account transcript using your smartphone. IRS2Go allows you to request this information, which will be mailed to you within several business days.

Free Tax Prep Providers

The IRS Volunteer Income Tax Assistance (VITA) and the Tax Counseling for the Elderly (TCE) Programs offer free tax help for taxpayers who qualify. You can use this brand new tool to help you find a VITA site right near your home. You simply enter your zip code and select a mileage range. To make it even more convenient if you click on the directions button within the results the maps application on your device will load with the address, making it easy to navigate to your desired location.

Stay Connected You can interact with the IRS by following us on Twitter, watching helpful videos on YouTube, sign up for email updates, or contact us.

Download the IRS2Go App

If you have an Apple iPhone or iTouch, you can download the free IRS2Go app by visiting the iTunes app store. If you have an Android device, you can visit Google Play to download the free IRS2Go app.

On December 19, 2014, President Obama signed into law The Tax Increase Prevention Act of 2014 (HR5771), which which temporarily extends over 50 expired incentives for individuals, businesses and energy through 2014. The law also creates Achieving a Better Life Experience (ABLE) accounts set up for the benefit of persons with disabilities. Extenders included in the legislation are the state and local sales tax deduction, IRA distributions to charity, and the above-the-line deduction for higher education.

Key provisions in the bill particularly impacting construction and real estate businesses include the extension of 50% bonus depreciation and qualified leasehold improvements for the 2014 tax year. Under HR 5771, qualified leasehold improvement property will continue to be eligible for 50% bonus depreciation. This property is defined in IRC 168(k)(3) as new improvements to an interior portion of a building that qualifies as nonresidential real property. In addition, this treatment is available as long as the improvements are made by the lessor more than three years after the date the building was placed in service.

Notable exceptions to qualified leasehold improvement treatment include: elevators, escalators, structural components benefiting a common area, or the internal structural framework of the building. For more information or to take advantage of the new legislation, please contact Eric L. Bach & Associates for a free consultation.

AUGUSTA, Ga. — The Masters green coat that came into vogue in the late 1930s has become what amounts to the world’s most recognizable reversible jacket. Augusta National Golf Club members wear theirs on the grounds to make themselves visible to tournament patrons seeking guidance on the course. And the reigning Masters champion wears it to make himself visible outside the club’s gates to anyone in search of a connection.

AUGUSTA, Ga. — The Masters green coat that came into vogue in the late 1930s has become what amounts to the world’s most recognizable reversible jacket. Augusta National Golf Club members wear theirs on the grounds to make themselves visible to tournament patrons seeking guidance on the course. And the reigning Masters champion wears it to make himself visible outside the club’s gates to anyone in search of a connection.